Europe - mixed plastic waste supply to further tighten

The European mixed plastic waste market is expected to further tighten in 2022 amid growing use of mixed-polyolefins grades by mechanical recyclers and increased use of refuse derived fuel (RDF)-suitable reject bales by pyrolysis-based chemical recyclers.

Mechanical recyclers are increasingly exploring the use of mixed-polyolefins waste as a feedstock, amid record high recycled polyethylene (R-PE) and recycled polypropylene (R-PP) pellet prices and structural shortages of mono-sorted R-PE and R-PP waste.

New sorting capacity from waste managers and recyclers targeting the use of mixed-polyolefins waste, is due to come on stream in 2022.

This is not the first time that mechanical recyclers have explored mixed plastic waste as a feedstock, with previous attempts unsuccessful because low yields and the complexity of sorting material made the process economically unviable.

Nevertheless, ongoing tight supply of mono-material bales and growing demand for recycled material have shifted the economic feasibility of using mixed plastic waste significantly.

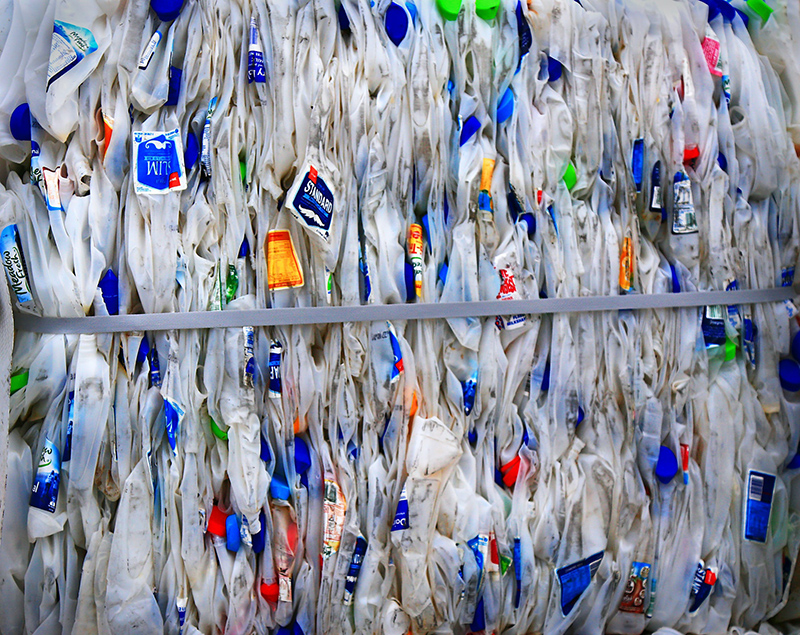

Single-material bale prices surge

With sharp increases in single-material bale prices across 2021, ongoing structural shortages, developments in sorting technologies, and firm recycled high-density polyethylene (R-HDPE) and R-PP pellet values (currently at record highs in Europe), using mixed polyolefins waste as an input has become economically viable.

Northwest Europe (NWE) post-consumer mixed coloured high density polyethylene (HDPE) bale prices increased by 393% on average in 2021. NWE PP post-consumer mixed-coloured bale increased by 182% on average in 2021. NWE colourless post-consumer polyethylene terephthalate (PET) bottle bale values increased by 131% on average in 2021.

With a number of new packaging projects scheduled for 2022 – driven by the ongoing sustainability pressure on fast moving consumer goods (FMCG) brands – mono-sorted HDPE and PP bale availability is expected to remain low throughout 2022.

Increasingly, waste managers and mechanical recyclers are looking to extract the usable polyolefins from mixed-polyolefins bales, leaving an RDF-suitable reject bale that can then potentially be sold onwards into the chemical recycling or RDF sector. RDF reject bales are currently selling at positive values.

Mixed-polyolefins bale supply to tighten

Mixed-polyolefins bale availability is expected to further tighten in 2022, particularly in France as a result of new mechanical recycling sorting and treatment capacity expected to come on stream in the first quarter of 2022.

High prices for mixed-polyolefins fractions and the desire to avoid competing with mechanical recyclers has meant that pyrolysis-based chemical recyclers are increasingly switching away from rigid and mixed-rigid/flexible grades of mixed polyolefins.

Historically, mixed polyolefins have been the preferred feedstock choice for pyrolysis-based chemical recyclers because of the need to limit PET (which oxidises, and does not depolymerise via pyrolysis), chlorine (which is corrosive), nylon and flame retardants content in its input material.

At the same time, high energy costs are making burn for energy more attractive and the RDF market is growing – particularly from the cement industry.

While most pyrolysis-based chemical recyclers are eager to avoid competition with mechanical recyclers for ideological reasons, this is placing them in direct competition with the RDF sector because of a lack of sufficient infrastructure to meet expected demand.

Although 2021 saw northwest Europeean RDF reject bales trading in positive territory for the first time, in some other European territories, such as Scandinavia and the Netherlands, prices continue to trade in negative territory, although this is expected to change as chemical recycling demand scales up in 2022.

There is currently 364,000 tonnes/year of operational chemical recycling capacity in Europe, of which 218,000 tonnes/year (or 60%) is pyrolysis based, data from the ICIS Chemical Recycling Supply tracker shows.

With new chemical recycling plant volumes frequently being announced, this volume is expected to increase in the coming years, even as the majority of plants remain at pilot or lab scale.

More on recycling